Will large-scale pharma M&A and licensing deals be the next major catalyst for psychedelics this year?

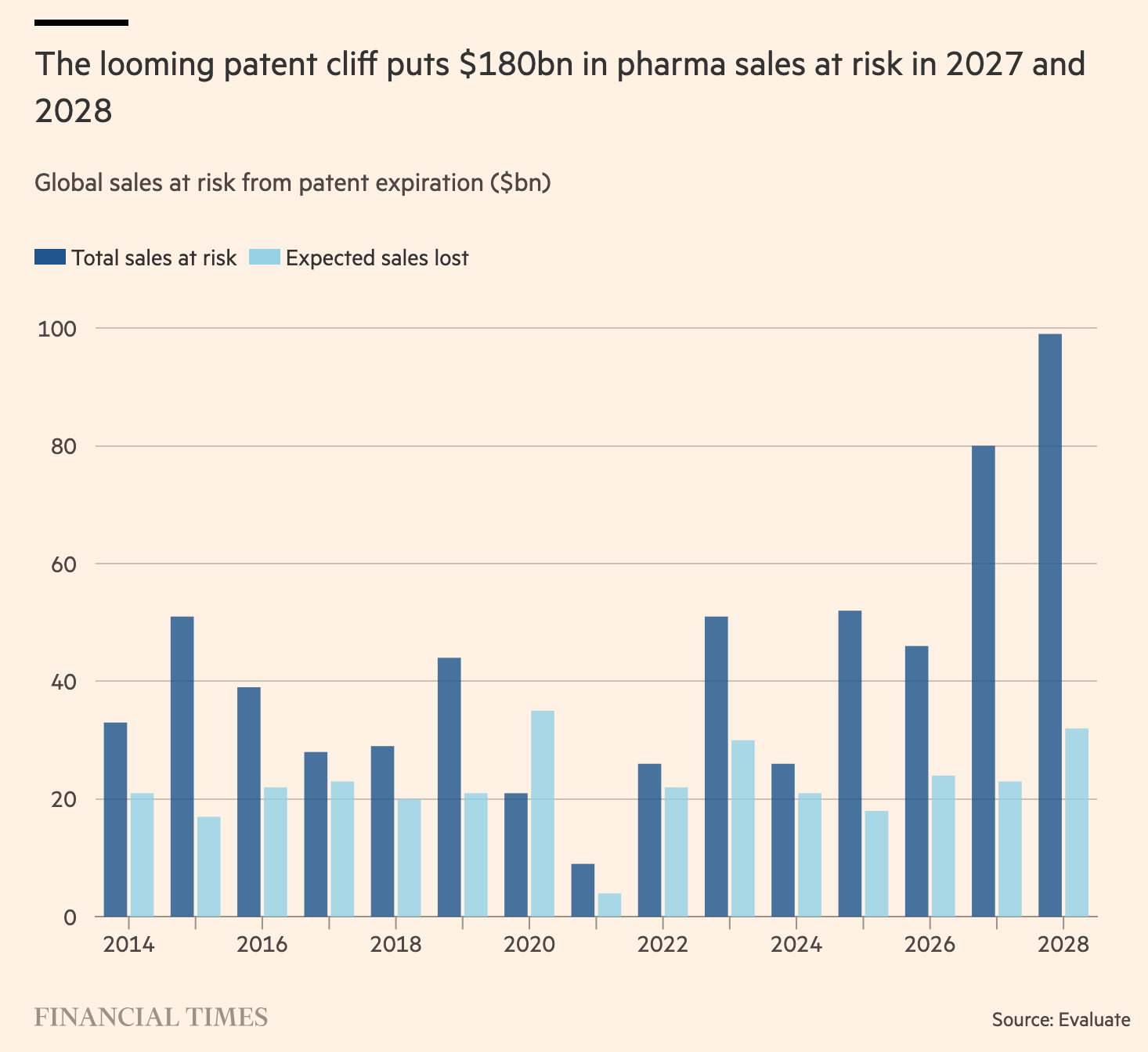

A massive upcoming patent cliff puts $180bn in big pharma sales at risk in 2027 and 2028

Over the last weeks, there was a lot of excitement and commentary on the recent positive regulatory, clinical and commercial momentum in the field of psychedelics and interventional psychiatry.

The consistent reiteration by the US Secretary of Health RFK Jr. and the FDA chief Marty Makary that they will treat psychedelics as a “top-priority” and work very hard to approve the first psychedelic within the next 12 months, the positive COMP360 Phase 3 and positive BPL-003 Phase 2b data readouts paired with the most recently announced 61% YoY growth in US sales of J&J’ Spravato to an annual run rate of $1.7bn has catapulted stocks of psychedelic drug developers up 50-150% over the last 3 months.

However, one topic has so far received very little attention and might drive stock prices of psychedelic drug developers up even further in the next quarters to come: Big pharma is facing massive patent cliffs for many of its multi-billion drugs in the upcoming years. The loss of exclusivity of many blockbuster drugs could evaporate a large junk of its current revenue streams as generics companies start entering the market. The below graph from a recent Financial Times article shows the dramatic magnitude of this looming patent cliff across all therapeutic areas: $180bn in pharma sales are at risk in 2027 and 2028 alone. Looking at the top five selling drugs in psychiatry alone reveals that ~$14bn in branded product annual sales are at risk over the next 5 years (see below for a more granular breakdown).

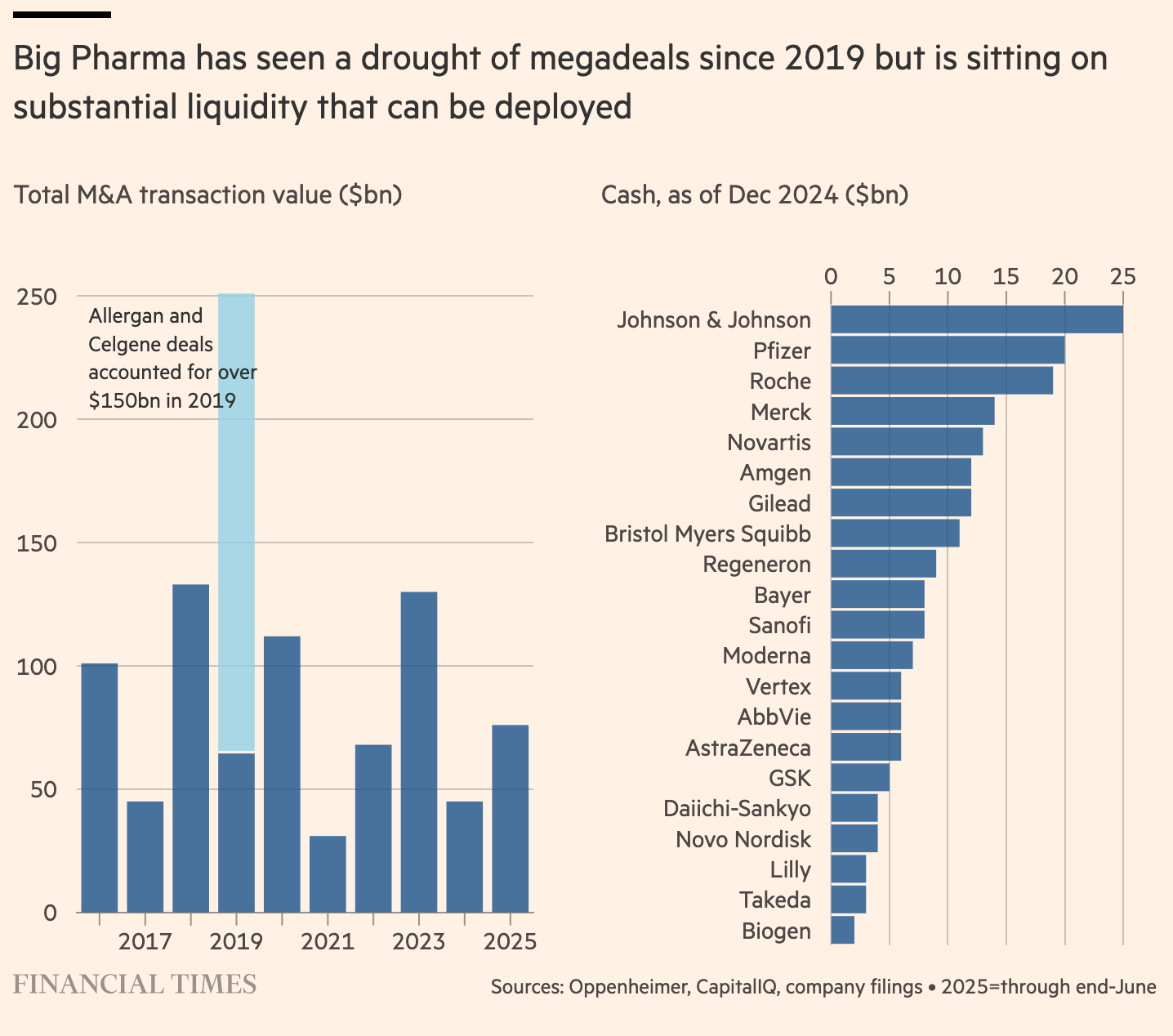

Given (1) the magnitude of the imminent patent cliffs (2) the significant cash reserves that commercial-stage pharma companies sit on (see second FT graph below) and (3) multiple psychedelic compounds now in Phase 2 and Phase 3 today, we had a closer look at publicly available data to determine, which psychiatry-focused large pharma companies with a current or planned commercial footprint are under pressure to make some M&A moves due to the upcoming loss of exclusivity of their high-revenue drugs over the next years. And - based on their public statements, cash reserves, strategic fit and activities in the psychedelics space to date - which of these pharma companies might be the first one to announce a major late-stage psychedelic deal, potentially as early as this year.

Lars and I plan to share a more detailed analysis over the next weeks, but here is already a sneak preview. This list of the top 5 psychiatry drugs ranked by sales in 2024 provides an overview of the expected patent cliff of each blockbuster drug in psychiatry (spoiler alert: first one hits already next year) and the companies that currently commercialize it (as you’ll see Spravato didn’t make the cut in 2024 yet but will likely be among the top 5 psychiatry drugs in 2025 based on its current run rate):

J&J: Invega Sustenna for Schizophrenia and schizo-affective disorder: ~$4.2bn, patent cliff 2030/31, sales started to decline.

AbbVie: Vraylar for Schizophrenia, bipolar I, adj. MDD: ~$3.3bn, patent cliff in 2028/29.

Otsuka & Lundbeck: Rexulti for Schizophrenia, adj. MDD, agitation in Alzheimer’s: ~$2.4bn, patent cliff 2028/29.

Otsuka & Lundbeck: Abilify Maintena/Asimtufii for Schizophrenia and bipolar I, ~$2bn (Maintena achieved peak sales $9.4bn in 2013, key patent expired in Q4’24), Asimtufii patent out to early 2030s might slow decline in sales.

Takeda & Lundbeck: Brintellix / Trintellix for MDD: ~$1.6bn, patent cliff in 2026.

While they have little to no commercial relevance in psychiatry (yet), given their renewed strategic focus on neuroscience and mental health, Novartis (its predecessor Sandoz discovered LSD decades ago), Boehringer Ingelheim and Bristol Myers Squibb are also worthwhile mentioning as potentially relevant (future) commercial-stage players in psychiatry. This list is focused on psychiatry only. As psychedelics hold great promise in neurology as well, we will also include companies that have relevant commercial-stage neurology assets in our deep dive in a few weeks.

Most of the commercial-stage companies above have gained exposure to “psychedelics-like” compounds in varying degrees over the last years. J&J has the lead (commercially) with its interventional psychiatry franchise Spravato that is now on an annual run rate of ~ $1.7bn and analysts and J&J forecast it to reach peak sales up to $5bn over the next years. Through its acquisition of Intra-Cellular Therapies earlier this year, J&J also has exposure to early-stage psychedelic-derived neuroplastogens.

Pharma companies (next to J&J) that were most active in the psychedelics space to date:

Otsuka: Among the first-movers in 2020 with Series B investment in Compass Pathways (NASDAQ: CMPS) along with atai Life Sciences. Collaboration in 2021 with atai Life Sciences (NASDAQ:ATAI) subsidiary Perception Neuroscience to develop R-ketamine. Mindset Pharma acquisition in 2023.

AbbVie: Largest headline deal number so far with up to ~$2bn (upfront, milestones and royalties). Option agreement in 2023 with the private biotech Gilgamesh to research and develop a portfolio of next-generation therapeutics for psychiatric disorders. Upon option exercise, AbbVie will lead development and commercialization activities.

Ferring Pharmaceuticals: Latest pharma company to enter the space with an investment in atai Life Sciences in 2025

Stay tuned for more detailed insights soon.

Additional Sources (not linked above):

| A guest post by

|